By Caesar Vallejos

OPEN FOR BUSINESS, Eagle News Service

The Philippines’ largest thrift bank, the BPI Family Savings Bank (BFSB), launched the one and only housing loan in the country that provides clients with a savings account.

The savings account is “on us, free – equivalent to P10,000 for every 1M housing loan and clients can choose from three deposit products” of the bank, BPI Family Savings President Ginbee Go announced in a media roundtable held at the Makati Shangri-La last March 19, 2019.

“We encourage Filipinos to do both: invest in housing loan and save, sooner rather than later, today rather than tomorrow,” Go said. “We will show Filipino families that it can be done,” she added.

Go cited the fact the Philippines’ gross savings rate is only 13.3% and only 26% of Filipinos have a bank account. “Having some savings can be a challenge given the day-to-day needs,” Go added.

“This is why through this program, our mission is to enable Filipinos to progress in life and achieve their dreams of having a home and being able to have some savings at the same time,” Go said.

In his presentation, BFSB VP Ramon Noel Altamirano detailed that a client who avails of a housing loan can earn up to Php100,000 in his savings account. “For every Php 1 million approved loan amount, a client will be given Php10,000 in a BPI Maxi Saver (with higher yielding interest) or Pamana Savings account (bundled with insurance coverage), up to Php 100,000 for a loan of at least Php 10 million. This will be made available after two months of amortization payments.

Inspired by Filipino aspirations

The BPI Family Savings President mentioned a National Economic Development Authority (NEDA) study in 2016 citing that four of five Filipinos aspire for a simple and comfortable’ life rather than a rich and extravagant life.

“This means having a medium-sized home, earning enough for day to day needs, having one car with financial capacity to send children to college and some money for local trips,” Go explained.

Go said that the NEDA study was consistent with the bank’s own research findings that “the that top three most coveted acquisitions for investments for Filipino families are owning a home; having a bank account and a car; and putting up their own business.”

Go also pointed out that “the reality is that is difficult to save enough to personally enjoy your dream home now given the faster appreciation of real estate prices versus one’s savings rate.”

“Getting a loan is not necessarily the preferred route for some if not many because of considerations such as fear of not being able to pay the loan or the fact that it adds expenses because they have to pay the interest on that loan,” she said.

However, Go emphasized that getting a housing loan is enabler to affording ones’ dream home. “A housing loan should be seen more as an investment,” Go said.

“Clients have to feel comfortable that they can meet their monthly obligations,” she added. The rule of thumb in deciding how much should be set aside for monthly amortization, according to Go, should not exceed 50% of one’s monthly income.

Reacting on how the unexpected rise in interest rates impact on home loans which had 175 basis points in rate increase last year, Go said, “at the end of the day it’s not the interest rates that is really the gauge by which consumers will avail. It’s the affordability of the monthly amortization.”

But Go was quick to point out that “now, we see a tapering off so we don’t really see a contraction particularly in housing loans. We’ve seen much higher interest rates in the past.”

Responsible financial management

That insight of wanting to provide for the family, to progress in life, through having a home and a bank account was BPI Family’s “inspiration for putting together this bundle of a housing loan and a deposit.”

The logical thinking is if one avails of a housing loan, he will also use up his savings. “That is not what we would want you to do. We are promoting responsible financial management and that’s why we say, ‘know what you can afford in terms of housing loan and we will show you how – just set aside 50% of your monthly income and that means you have enough for day-to-day and have enough for your savings and we will help you with the seed money for a deposit account,” Go said.

Housing backlog and financial inclusivity

BFSB has projected a 10-15% for total loan growth, both for auto and housing. “We were flat last year on our total loans because we were in the mode of testing and refining our processes which had been unresponsive already given the size of our business. We’ve doubled our business in the last five years from 2012 to 2017 and therefore we really have to make sure that our processes will remain to be streamlined and competitive,” Go said.

Go cited that “the 4 million housing backlog can actually go about to about 6 million because of the demand for more housing in the future by 2030 given the rapid urbanization of the country and the growing population.”

“What are we doing with the economic and socialized housing is to work closely with developers,” Go said. Her team is also testing and studying these sectors to develop a program for these markets.

“Our desire is to be really more financially inclusive,” Go said. “When you talk about inclusivity, it really is based on income levels, so we look at affordability and accessibility.

We need to be able to provide them with products that allow them to access financial institutions at more affordable ways one of which is through the payments,” Go said.

She explained that encouraging Filipinos to transact using payment facilities of banks, that already helps them begin their journey towards banking. “It’s really providing them with the confidence that they need that so they can be part of the ‘bankable’ market.

Aside from access and affordability, the other critical factor in financial inclusion is technology as an enabler.

“There are a number of fintechs for payments…and the mobile device is becoming a very powerful banking tool. Being able to transact using the mobile will certainly be an enabler towards more financial inclusion and getting more and more people banked,” Go stressed.

Finally, Go said that policy regulations must be friendlier to those who are in the lower income. “We are looking at how we can make banking more accessible through easier documentary requirements and easier opening of bank accounts.

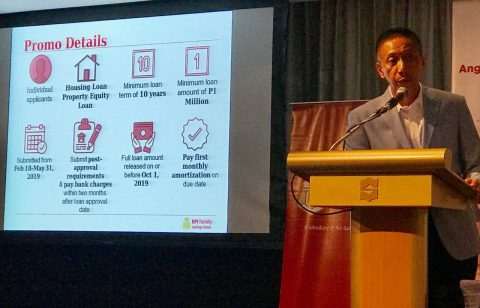

The Family Housing promo is available until May 31, 2019 only.